NGUYÊN NHÂN CAO SU KHÔNG NGỪNG GIÀM GIÁ

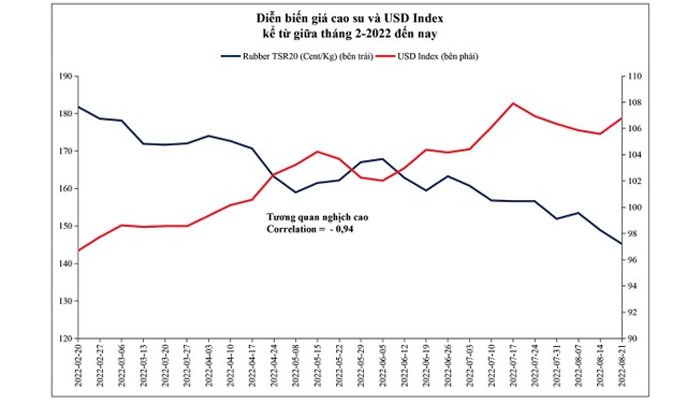

Tính tới ngày 26-8, giá cao su TSR20 kỳ hạn tháng 9 trên sàn SICOM giao dịch quanh mức 143 cent/kg, tương ứng giảm 23,9% kể từ mức đỉnh ngày 19-1. Trên sàn Thượng Hải và sàn OSE (Nhật Bản) cũng chứng kiến xu hướng giảm liên tục đến nay, với mức giảm lần lượt 17,5% và 23,4%.

1. Nguyên nhân cao su giảm giá liên tục

Nguồn cung cao su tự nhiên không bị tác động gián đoạn bởi cuộc chiến Nga - Ukraine do chủ yếu tập trung ở các nước Đông Nam Á như Thái Lan, Indonesia, Việt Nam, Malaysia, với tỷ trọng ước tính trong năm 2022 lần lượt 34%, 22%, 9% và 3% thế giới. Báo cáo của Sri Trang cho biết, sản lượng cao su tự nhiên của thế giới trong năm nay dự kiến đạt 14,27 triệu tấn, tăng 3,5% so với mức sản lượng 13,79 triệu tấn của năm ngoái. Trong đó, sản lượng của hầu hết quốc gia nằm trong top 10 đều dự kiến tăng trưởng tốt, như Thái Lan tăng 3,1%, Indonesia tăng 4,6%, Việt Nam tăng 1,5%, Trung Quốc tăng 6,8%.

Với nguồn cung thuận lợi nhưng giá cao su lại chịu tác động tiêu cực từ phía nhu cầu bị gián đoạn hoặc suy yếu, cùng các yếu tố định giá khác như USD Index và dầu thô. Nhu cầu tiêu thụ của Trung Quốc chiếm tới 41% thị trường cao su tự nhiên thế giới, tuy nhiên nền kinh tế nước này liên tiếp đối diện với các trở ngại trực tiếp và gián tiếp, như thị trường bất động sản trước rủi ro vỡ nợ, phong tỏa phần lớn thời gian trong quý II bởi dịch bệnh. Đặc biệt, sự tăng giá của USD so với đồng NDT và THB (baht Thái Lan) đã thúc đẩy xu hướng giảm giá cao su tự nhiên, bởi các nhà xuất khẩu Thái Lan (chiếm 34% nguồn cung) có nhiều dư địa hơn để giảm giá bán cạnh tranh thị phần. Trong bối cảnh sức mua từ các nhà nhập khẩu Trung Quốc suy yếu bởi kinh tế trì trệ và đồng NDT mất giá.

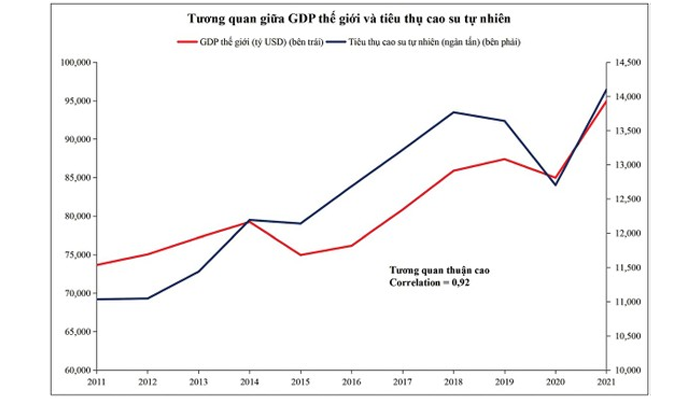

Giá dầu thô bắt đầu giảm kể từ đầu tháng 6 đến nay cũng góp phần ảnh hưởng đến giá cao su tự nhiên. Mối tương quan thuận đo được giữa giá dầu WTI và cao su tự nhiên từ năm 2010 đến năm 2021 là 0,84. Điều này được hiểu do sự cạnh tranh với cao su tổng hợp được làm từ dầu thô chiếm tới hơn 50% thị trường cao su nguyên liệu. Không chỉ nhu cầu suy yếu ở Trung Quốc, nền kinh tế Mỹ cũng chứng kiến tăng trưởng âm trong 2 quý liên tiếp. Với động lực tăng trưởng yếu ớt từ 2 nền kinh tế lớn nhất thế giới, các tổ chức dự báo liên tục điều chỉnh giảm tăng trưởng GDP toàn cầu trong năm nay. Và nhu cầu tiêu thụ cao su tự nhiên có mối tương quan thuận cao với GDP, thể hiện qua hệ số correlation = 0,92.

2. Động lực tăng giá đến từ ngành ô tô?

Sử dụng cho lốp xe chiếm tới hơn 45% nhu cầu tiêu thụ cao su tự nhiên thế giới. Do đó, cần quan sát diễn biến tăng trưởng từ phía ngành ô tô. Hiệp hội ngành công nghiệp ô tô của Trung Quốc trong tháng 7 đã cắt giảm dự báo tăng trưởng doanh số bán ô tô xuống còn 3%, thay vì 5,4% như dự báo trước đó. Số lượng xe ô tô dự kiến bán được 27 triệu chiếc trong năm nay, tăng khoảng 3% so với 2021. Tín hiệu tích cực đối với thị trường ô tô Trung Quốc bắt đầu từ tháng 6 khi ghi nhận 2 tháng tăng trưởng mạnh liên tiếp. Số lượng ô tô bán được trong tháng 6 và 7 lần lượt 2,5 và 2,44 triệu chiếc, tương ứng tăng 24% và 30% so với cùng kỳ 2021. Như vậy, thị trường ô tô Trung Quốc được kỳ vọng tăng trưởng mạnh mẽ hơn, bù đắp cho khoảng thời gian phong tỏa bởi dịch bệnh trong quý II. Nhu cầu sẽ tăng dần vào những tháng cuối năm do đặc điểm chu kỳ GDP của Trung Quốc mạnh vào quý IV. Sự khởi sắc của ngành công nghiệp ô tô cũng diễn ra ở nhiều quốc gia như Ấn Độ, Việt Nam, Philippines, với số lượng xe bán được tăng trưởng lần lượt 51%, 34%, 27% so với cùng kỳ năm ngoái.

Như vậy, thị trường ô tô Trung Quốc được kỳ vọng tăng trưởng mạnh mẽ hơn, bù đắp cho khoảng thời gian phong tỏa bởi dịch bệnh trong quý II. Nhu cầu sẽ tăng dần vào những tháng cuối năm do đặc điểm chu kỳ GDP của Trung Quốc mạnh vào quý IV. Sự khởi sắc của ngành công nghiệp ô tô cũng diễn ra ở nhiều quốc gia như Ấn Độ, Việt Nam, Philippines, với số lượng xe bán được tăng trưởng lần lượt 51%, 34%, 27% so với cùng kỳ năm ngoái.

Tuy nhiên, ngành ô tô ở Mỹ và khu vực EU thể hiện sự trái ngược. Trong tháng 6, EU ghi nhận số lượng xe bán thấp nhất kể từ năm 1996 trở lại đây, với chỉ hơn 1,06 triệu chiếc. Đó là tháng thứ 12 liên tiếp ghi nhận số lượng bán xe suy giảm bởi vấn đề kinh tế trì trệ do Covid và cuộc khủng hoảng chip bán dẫn kéo dài. Số lượng xe bán lũy kế 7 tháng năm 2022 ở Mỹ cũng ghi nhận suy giảm rõ rệt so với 2021. Như vậy, có thể thấy kỳ vọng nhu cầu hồi phục từ ngành ô tô rất bấp bênh, bởi nền kinh tế EU dự kiến còn tiếp tục bị ảnh hưởng tiêu cực từ việc giá năng lượng quá cao, trong bối cảnh NHTW châu Âu (ECB) vừa bắt đầu lộ trình tăng lãi suất trong tháng 7. Niềm hy vọng lớn nhất là Trung Quốc có thể hoạt động kinh tế bình thường trở lại, bởi nhu cầu tiêu thụ ô tô nước này có thể bù đắp tương đương với tổng nhu cầu của Mỹ và EU. Khi đó, tăng trưởng nhu cầu chung toàn ngành ô tô sẽ phụ thuộc vào các quốc gia còn lại.

Cục Dự trữ Liên bang Mỹ (Fed) vẫn phát đi thông điệp sẵn sàng hành động mạnh tay hơn để kéo nhu cầu về sát với nguồn cung, nhằm ngăn chặn lạm phát vượt quá tầm kiểm soát. Điều này tạo động lực tăng giá cho USD tiếp tục diễn ra trong khoảng thời gian nữa. Đây là yếu tố gián tiếp gây bất lợi cho giá cao su tự nhiên, bởi nó làm suy yếu cơ hội tăng trưởng trở lại của nền kinh tế Mỹ trong thời gian tới. Với các diễn biến hiện nay, cơ hội tăng giá cho cao su tự nhiên rất thấp, đà giảm vẫn tiếp diễn ít nhất đến khi Fed hoàn tất lộ trình tăng lãi suất của mình.

>> Xem ngay các bài báo tin tức thị trường mới nhất chúng tôi cập nhật <<< />pan>

Mọi thông tin vui lòng liên hệ:

Ban Biên tập Mega Việt Nam

Địa chỉ: Tầng 2-A2-IA20, KĐT Nam Thăng Long, đường Phạm Văn Đồng,

Đông Ngạc, Q. Bắc Từ Liêm, TP. Hà Nội, Việt Nam.

Email: contact@megavietnam.vn

Tel: (+84) 24 375 89089; Fax: (+84) 24 375 89098

Website: megavietnam.vn

Hotline: 1800.577.728; Zalo: 0971.023.523